The price index fell slightly following the latest auction results due to a sharp decline in milk powder prices, as inventories accumulate amid temporary global raw milk overproduction. However, a modest recovery in fat and Cheddar cheese prices prevented a more significant drop in the GDT index.

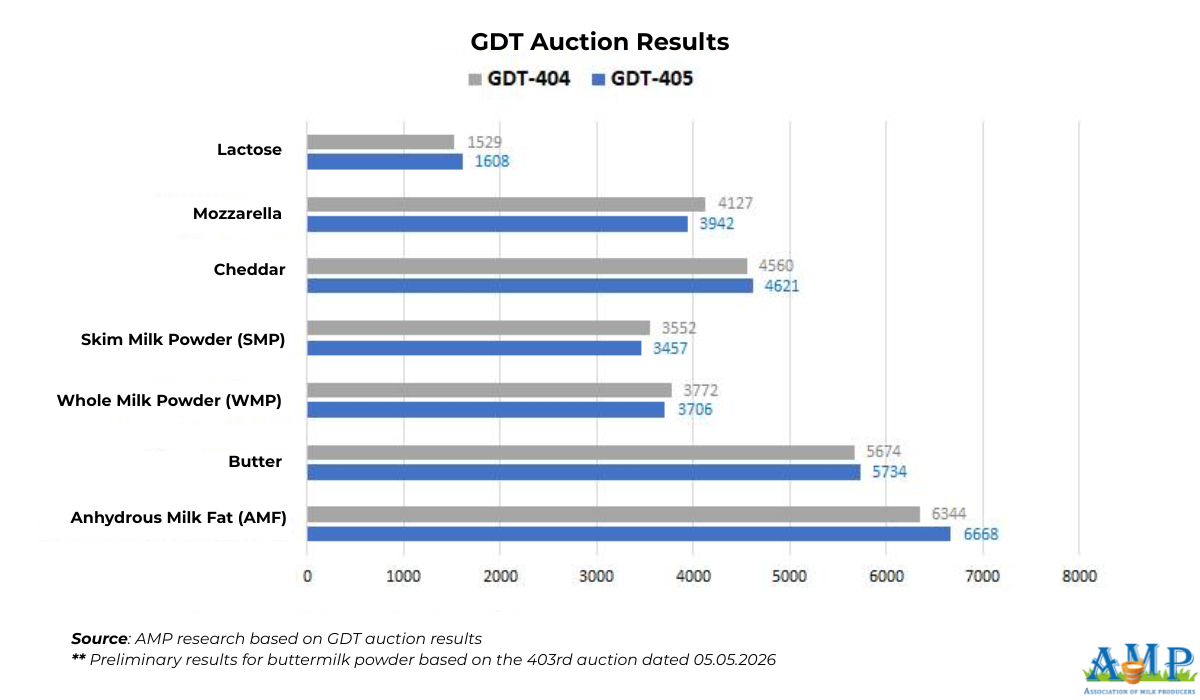

On Tuesday, June 2, the 405th GDT Auction took place, resulting in a price index of 1214, which is 7 points (-0.6%) lower compared to the previous auction. The average price for dairy products was 4,021 USD/mt, down 177 USD from the previous auction results. During the auction, 14,364 tons of commodities were sold, which is 1,392 tons more than the last auction. The minimum supply was recorded at 13,601 tons, and the maximum at 17,661 tons. 147 dairy market operators participated in the auction, which is 7 companies fewer than on May 19.

According to the results, the price for Anhydrous Milk Fat (AMF) was 6,668 USD/mt, up 5.3% compared to the previous auction. According to EDairy News, despite global raw milk overproduction, export market demand for dairy ingredients remains substantial, driven by intensified purchasing from food processing enterprises. According to the GDT forecast, AMF prices may increase by 3.2% in July and by 8% in August.

The price for Butter at this auction was 5,734 USD/mt, up 1.2% compared to the previous auction. According to Farmers Journal, butter prices strengthened in New Zealand last week. As reported by EDairy News, despite the increased product availability, buyers are still actively purchasing butter. According to the USDA, U.S. butter demand has slowed down following the April surge and remains at a stable level. Export market demand for butter is also stable, though competition in these markets is quite intense.

Due to the new EU trade agreement with Latin American countries and the introduction of duty-free tariffs on dairy products from the U.S. under pressure from the Trump administration, competing in the European market is becoming increasingly difficult. Unsold butter surpluses exist even in Switzerland, a country that previously did not face dairy marketing challenges. The Swiss government is considering state interventions to purchase butter to relieve market pressure and prevent a sharp drop in raw milk prices. Auction organizers expect the butter price to increase by 0.3% in July and by 2.4% in August.

The price for Whole Milk Powder (WMP) was 3,706 USD/mt, a decrease of 2.2% compared to the previous auction results. Competition in milk powder export markets remains intense amid a temporary increase in milk yields across various regions of the world. The balance of supply and demand in the dairy market remains quite fragile under the influence of high energy prices, geopolitical disputes, and rising inflation. Substantial milk production volumes could pressure prices if consumer demand in export markets slows down. According to EDairy News, despite increased product availability, export market demand for milk powder still remains significant. Auction organizers forecast a price decrease of 1.2% in July and 1.1% in August.

The price for Skim Milk Powder (SMP) was 3,457 USD/mt, down 3% compared to the previous results. According to the USDA, SMP inventories are gradually increasing in the U.S. on the back of slowing export demand, partly due to reduced purchases from Mexico. Domestic demand in the U.S. market has weakened, with buyers purchasing SMP in small volumes to cover only immediate needs. As reported by Farmers Journal, SMP prices weakened in New Zealand last week. According to Ornua, SMP prices are expected to rise in the near term; demand for SMP is quite strong, and European-produced commodities are currently cheaper than those from other producing regions. According to the GDT forecast, SMP prices may decrease by 1.6% in July and 3.3% in August.

Cheddar cheese rose to 4,621 USD/mt (+1.8%), while Mozzarella fell in price to 3,942 USD/mt (-4.6%). (Note: The original Ukrainian text says "подешешав до... (+1.8%)", which is a typo in the percentage/trend indicator; the translation corrects this to "rose to"). According to the USDA, American cheesemakers are channeling surplus raw milk into cheese production. Cheese demand has stabilized in the U.S. and export markets, with retail network sales outpacing sales to the food processing segment. Contract negotiations for U.S. and European cheese deliveries are dragging on due to additional logistics costs arising from ongoing shipping disruptions caused by the Middle East conflict. Meanwhile, cheese demand remains active in Southern European countries with the start of the tourist season.

The price gap between European and American cheeses is beginning to narrow. As Ornua forecasts, cheese prices could weaken in the coming weeks if production volumes continue to grow and oversupply the market with finished products. At the same time, according to EDairy News, despite surpluses in the dairy market, cheese demand remains substantial. Organizers expect Cheddar to increase by 1.9% in July and 3.1% in August, while Mozzarella may decrease by 4.6% in August.

Lactose increased to 1,608 USD/mt (+4.6%). According to the USDA, the upward trend in lactose prices continues due to active demand and limited product availability on the spot market. Lactose manufacturing is stable, and clients are securing contracts for finished product deliveries for the third quarter. According to the GDT forecast, lactose may rise by 4.6% in August.

Buttermilk Powder (BMP) rose to 3,578 USD/mt (+3%). According to the USDA, the price increase occurred amid tight supply, as processors focused on manufacturing skim milk powder, which is also a co-product of butter production. Organizers expect BMP to rise by 5% in July and 2.8% in August.

The next GDT Auction will take place on June 16.

Press service of the Association of Milk Producers

Follow us on LinkedIn

Related News