Despite the decrease in prices for milk raw materials in Europe, too much export supply for dairy products and weak demand on foreign markets, attractive niches for producers and exporters still remain in some countries.

Despite the decrease in prices for milk raw materials in Europe, too much export supply for dairy products and weak demand on foreign markets, attractive niches for producers and exporters still remain in some countries.

Production of raw milk by the main dairy regions

As of the beginning of 2023, there is a surplus of raw milk in Europe, while in Australia and South America, on the contrary, there is a significant shortage of supply. Despite the increase in milk production in New Zealand and the USA in January, milk production is expected to decrease until the end of the year due to unfavorable weather conditions, higher feed prices, a decrease in the number of cows, consumer inflation and weak demand for dairy products in the world, above all in China.

Europe. Throughout February, a large surplus of raw milk supply from farmers was observed on the EU market. The demand for raw milk in the member countries continued to decrease due to the approaching seasonal peak of raw milk production at the beginning of spring and due to a reduction in the supply of dairy products to domestic and foreign markets. According to the preliminary forecasts of the European Commission, in 2023 in the EU milk production is expected to decrease by 0.2% against the background of a reduction in the number of cows, an increase in the cost of milk production and a weak demand for dairy products on foreign markets.

European farms and dairies are feeling the effects of last year's "overheating" of the dairy market. In the first half of 2022, European producers significantly raised purchase prices for raw milk under the influence of a reduction in its production in Europe and Oceania. Europeans predicted a significant demand for dairy products in China after the lifting of quarantine restrictions. However, in February, demand in China was lower than expected. During the quarantine, the Chinese reduced their consumption of drinking milk, and local producers used surplus raw materials for the production of milk powder. Due to this, the stocks of this product in China have increased significantly. Demand for dairy products in Southeast and North Asia remains limited, unlike last year. In Japan, due to low milk prices and weak demand, farms are closing.

In February, European companies directed surpluses of cheap milk to the production of cheese and butter, focusing on demand in China, the United States and Oceania. However, the market quickly became saturated with these products. It is noteworthy that the Dutch company FrieslandCampina closed its butter production facilities in Rotterdam and Friesland, sold a production line in China and plans to close another factory in Hertogenbosch by mid-2025.

There is a stable demand for milk powder in Algeria, Brazil and Malaysia, but this is not enough to improve the situation on the European market. At the beginning of March, warehouses in Europe were filled with milk powder, cheeses and butter, which have nowhere to sell.

Australia. In Australia, on the contrary, processors experienced a shortage of raw milk in February. According to the estimates of the European Commission, 715 thousand tons of milk were produced in Australia in January. According to the Rural Bank, in January, the volume of milk production on the green continent decreased by 12% compared to December and by 6.6% compared to last year's season. According to the estimates of the owner of the Canadian company Saputo Lino, Saputo Jr., from 2001 to 2023, the volume of milk production in Australia has decreased from 11 to 8.5 million tons per year. The reasons for the reduction are unfavorable weather conditions, lack of qualified workers, reduction of agricultural land and mass closure of dairy farms.

From 1986 to 2022, the number of dairy farms in Australia fell from 22,000 to 4,400. Farmers are going out of business or switching to beef production due to rising water and feed prices, which account for more than 60% of the cost of milk production. The US Department of Agriculture predicts a reduction in milk production in Australia to 8.4 million tons in 2023. Due to the shortage of raw milk, large processors are forced to reduce capacity in the Australian market. For example, the Saputo company is closing its factory in Mafra, as well as reducing the staff at enterprises in Leongat, Mil-Lel, in order to optimize production processes.

Australia is reducing production of skimmed milk powder under the influence of limited demand in foreign markets. Australian producers use raw milk for the production of cheeses that are in demand in the domestic market. The Saputo company plans to invest 14 million dollars in transferring the production of cream cheese from the city of Mafra to Smithton. Domestic demand for dairy products in Australia remains strong. According to the NielsenIQ Homescan survey, 97% of Australian households continue to buy dairy products despite rising prices.

New Zealand. According to the European Commission, in January, New Zealand farmers milked 2.35 million tons of milk, which is 1.2% more compared to the same period last year. However, New Zealand dairy cooperative Fronterra predicts a reduction in milk production until the end of 2023 due to the negative effects of Cyclone Gabriel on the dairy industry, weakening demand for whole milk powder in China.

USA. Raw milk production in the US at the beginning of the year remains stable and covers the needs of dairies. According to the US Department of Agriculture, milk production was expected to increase by 2.23% in February compared to January. According to preliminary estimates of the European Commission, in January the USA produced 8.75 million tons of milk, which is 1.3% more than a year ago. The Ministry of Agriculture forecasts an increase in the production of raw milk by only 0.88%, which is due to a reduction in the number of cows, drought, higher prices of feed and limited demand for dairy products in China.

In the US domestic market, the consumption of dairy products decreased by 1.4% compared to last year. This is especially true for skimmed milk powder (-1.6%). In the American market, there are expectations of the activation of the restaurant business, which should contribute to the reduction of surplus cheeses in the domestic market. According to the forecast of the National Restaurant Association, American restaurants can increase their revenue by 58% in the first half of 2023.

In January, the US increased the volume of exports of dairy products by 16%. Supplies of cheese, dry whole and skimmed milk, and whey increased the most. A lifeline for American dairy farmers was neighboring Mexico, where the economic situation is improving and demand for food industry products, including milk powder and cheeses, is growing.

South America. In the region, the volume of milk production is decreasing due to insufficient feed supply. The quantity and quality of crops has been falling for several years in a row due to drought in the agricultural regions of Argentina, Brazil and Uruguay. In Brazil, there is a stable demand for whole milk powder. Cream cheese is also in demand in South American countries. In 2022, the number of new cream cheese factories in the region increased by 10% compared to 2021.

Prices and trends of the world dairy market

Raw milk prices vary in different regions. According to IFCN's forecast, in 2023, the prices of milk raw materials will be affected by inflation, recession, an increase in the cost of production due to the increase in the price of fuel, electricity, feed and fertilizers, and a reduction in the purchasing power of consumers in certain regions.

In most European countries, raw milk prices continue to decline due to large oversupply and limited market demand. In February, the average price for raw milk in the EU fell by 2.79%, to 54.78 euro cents per kg, compared to January. At the same time, the cost of milk production on farms is increasing due to the increase in the price of feed, fuel and fertilizers, as a result of the full-scale invasion of russia into Ukraine, the destruction of logistics chains and restrictions on European-Russian trade.

The lowest prices were reached in Poland and the Baltic countries. In February, the price of raw milk in Poland decreased by 11.19% (to 46.4 euro cents/kg), in Lithuania – by 18.16% (to 37.55 euro cents/kg), in Latvia – by 14.77% (up to 37.37 Eurocents/kg).

Agnieszka Malyszewska, vice-president of the confederation of Polish agricultural cooperatives COGECA, comments that for many farmers, milk production becomes unprofitable, and processors incur huge costs for electricity, packaging and labor. In her opinion, there are risks of bankruptcy of dairies and cooperatives in Poland. The director of the Association of Milk Producers of Lithuania, Eimantas Bičius, said that the prices of milk in his country fell below the cost price. During February, Lithuanian farmers staged protests outside supermarkets against low prices, gave away free or even poured devalued milk.

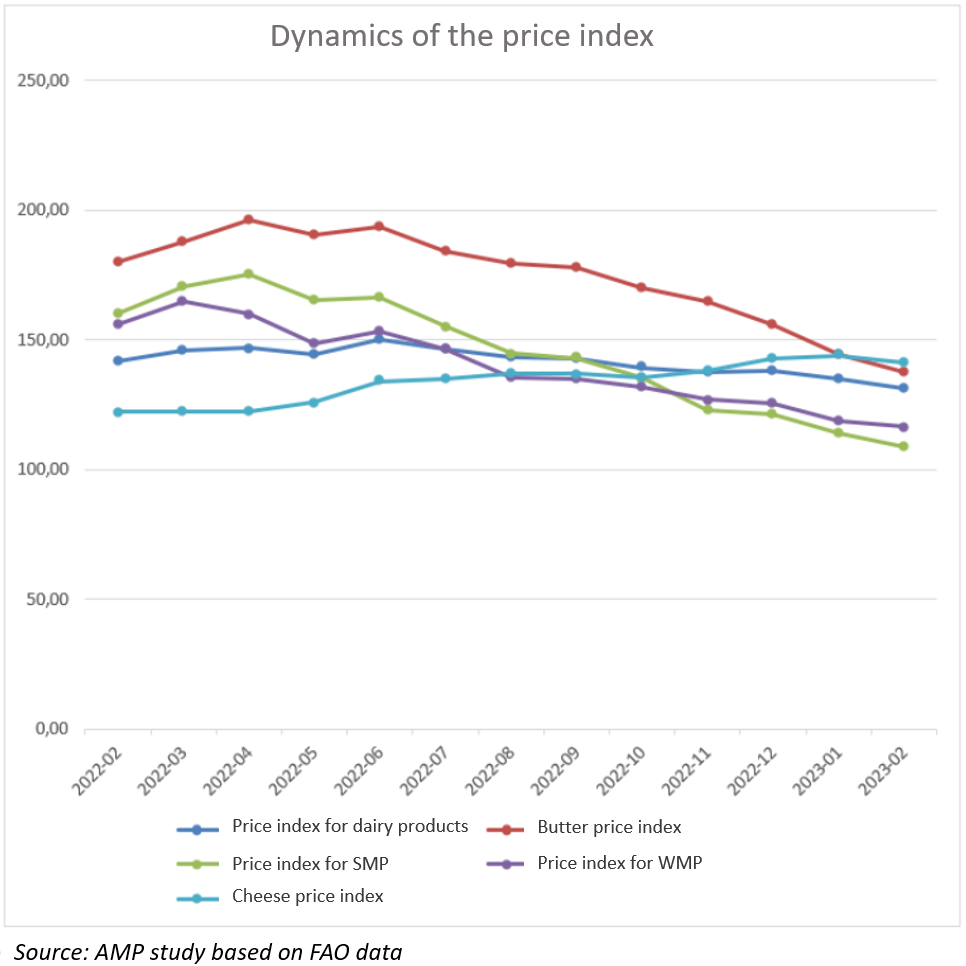

Adding fuel to the fire is weak demand for dairy products in foreign markets, as evidenced by the results of the latest GDT trades. The average price of dairy products decreased by 0.7%. The price of all dairy products has fallen, with the exception of dry whole milk and lactose. In February, the average value of the FAO Dairy Price Index was 131.3 points, which is 3.6 points lower than in January and 10.2 points lower than the February 2022 level. As noted by the FAO, one of the reasons for the reduction in prices for dairy products is the increase in the export supply of butter, cheese and skimmed milk powder in Western Europe.

In New Zealand, companies are cutting forecast milk prices due to weak demand for whole milk powder in China. In March, Synlait lowered its price expectations for 2023 from NZ$9 to NZ$8.5 per kilogram of milk solids (-5.5%). In February, the Fronterra cooperative refrained from raising the price above NZ$9. The cost of milk production in New Zealand is affected by the importation of coconut kernel feed from Indonesia and Malaysia, which is the main foreign additive in animal diets.

In Australia, on the contrary, milk prices are rising due to limited supply in the domestic market. According to Dairy Australia, dairy prices in Australia are higher than in other regions. The Australian Dairy Farmers Corporation has raised the price of milk by almost 4% for the period from January to June 2023. In December, the price was 10.05 Australian dollars per kilogram of dry milk residue, but the company's management decided to increase it to 10.45 Australian dollars.

In South America, raw milk is also rising in price due to limited supply from local farmers. According to Clal.it, in January the price of raw milk in Argentina amounted to 35.73 euro cents per kg, which is 5.65% more than in December, in Brazil - 47.49 euro cents per kg (+5.57%) , in Uruguay – 38.77 euro cents per kg (+1.48%).

Raw milk is getting cheaper in the US. According to Clal.it, raw milk in America cost $23.10 per 100 pounds (€47.29 per 100 kg) in January, down 6.48% from December. The USDA predicts a $0.25 drop in milk prices in 2023.

At the same time, the cost of milk production in the United States is increasing due to the increase in the price of such feeds as alfalfa hay, corn, soybean meal, and the increase in the price of young animals. The reasons are a reduction in corn and soybean harvests last year, as well as a reduction in the cattle population. Drought is a challenge for American forage producers.

From February 4 to March 4, prices for skimmed milk powder and cheddar cheese decreased slightly (-0.1%), but butter rose slightly (+0.06%), according to the USDA. Rising commodity prices in the US are restraining weak demand in foreign markets.